Carbon Capture and Storage - filling in the gaps of clean energy

Kari Forthun, Project Manager R&D at FTG

FTA Issue No.2 2025

What do we do with our trash and wastewater?

We collect it, treat it, and dispose of it safely. But what about our carbon dioxide (CO₂) emissions – our invisible waste? For decades, we have been freely dumping CO₂ into the sky from massive use of fossil fuels, leading to climate change.

Imagine if we considered CO₂ like our trash or sewage – would we still dump it freely into the sky?

Carbon Capture and Storage (CCS) is waste management - the climate mitigation technology whereby CO2 is treated as waste and disposed of in a responsible way.

This article can be downloaded as a PDF at the Fjell Tech agenda homepage - Download center.

Electrify anything that can be electrified

Cutting emissions directly should be priority number one – by use of renewables instead of burning fossil fuels, and by improved energy efficiency. Also, not emitting simply by reduced consumption is the elephant in the room that must be addressed – our consumption is the sole purpose of all production and emissions in the first place.

Why not stop using fossil fuels and avoid CO₂ entirely?

CCS is not a substitute for replacing fossil fuels; it’s an added tool and measure that handles emissions from activities we cannot easily remove, electrify or replace. CCS enables economies to keep using essential, heavy industries without releasing CO₂ emissions. Cement production, chemicals production and steel mills are examples of industrial sources with CO₂ emissions where CCS has a role to play. These industries produce CO₂ as a by-product in their processes.

Another example is in electricity production. In an energy mix dominated by renewables, CCS on gas power plants can provide back-up power to the grid in periods when there is little wind and sunshine (low renewable electricity production).

Smoke from factory pipe of heat station in a city in wintertime. CO2 is an invisible gas, the white air pollution is evaporated water that condenses into tiny water droplets, like fog or a cloud

What is CCS and how does it work?

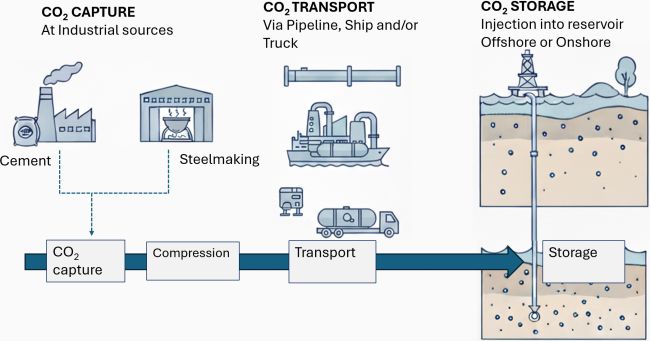

Instead of letting CO₂ from factories and power plants pollute the atmosphere, CCS is a set of technologies that capture CO₂ at the source, transports it (via pipelines, ships or trucks), and stores it deep underground.

CO₂ can be captured and filtered out from the exhaust gases at facilities like power plants, cement furnaces, steel mills, or chemical plants. This is typically done with special solvents or membranes that absorb or separate out the CO₂.

The predominant capture method today takes place in a two-step cycle. In the first stage, CO2 is captured by a solid or liquid absorbent. In a second stage, the CO2 is released by changing either temperature or pressure, whereby the reaction is reversed to release the CO2. Once the CO2 is released, the absorbent is recycled back to the first stage for more capture. Membranes can also be used by allowing CO2 selectively to pass through the membrane faster than other gases.

Once CO₂ is captured and compressed into a fluid, it needs to be transported to a storage site. The cheapest way is usually via pipelines, there are already > 8000 kilometres of CO₂ pipelines in U.S. (initially built for the oil industry). Ships and trucks can carry liquefied CO₂ when pipelines are not feasible, for smaller volumes, or when sea transport is more beneficial.

Schematic illustration of the CCS value chain. CO2 is captured at the emission point, pressurized, transported via pipeline, ship and/or truck and injected into a storage site in the subsoil permanently, either offshore or onshore

The pioneering Northern Lights project ships CO₂ from European industries to a receiving terminal whereby CO₂ is transferred via pipeline to an offshore well for storage. The final step is pumping the CO₂ deep underground into rock formations that keep it trapped. The first CO2 was successfully injected into Northern Lights JV storage site in August 2025 [1], marking a true world event for climate action.

Ideal storage sites are often depleted oil & gas fields or deep saline aquifers (porous rock layers filled with brine), typically a few km below ground. At these depths, CO₂ acts like a dense fluid, trapped under thick cap rock layers. Over time, it can slowly dissolve or even mineralize (turn into carbonate rock). Storage is designed to be permanent – comparable to how natural gas has stayed trapped in reservoirs for millions of years (until we drilled for them).

The ship Northern Pioneer at CO2 receiving facilities of Northern Lights JV in Øygarden, Norway. Photo by Ruben Soltvedt. News and media archive - Northern Lights. Northern Lights JV is one part of the government funded Longship project that build a full CCS value chain.

Who pays to clean up our emissions?

CO₂ waste management has lacked enough incentives to enable large-scale use. Market forces are designed insufficiently, and CCS has been prevented by emissions not being priced correctly. CCS is therefore a policy-driven technology. Policy uncertainty is even considered to be the biggest barrier today to CCS deployment, and one of the key reasons for CCS projects failing in the past [2]. CCS is a supporting service industry lacking a business case that can fly on its own. There are three dominant ways in which policymakers make CCS happen.

- Carbon pricing – the “Stick” that push reductions. EU’s Emissions Trading System (ETS) is an example where the carbon price today is around €65–100 per ton of CO₂. expected to increase substantially ahead [3].

- Incentives and Subsidies – the “Carrot” that pull reductions. Providing tax credits, grants, funds or contract-for-difference models (guaranteed price for stored CO₂).

- Strategic Public Investments: Governments directly fund large parts of CCS projects. The state of Norway has covered 70-85% of the cost of various parts of the Longship value chain. An analogue can be made to public investment in infrastructure whereby road or sewage systems are funded to support a kick-start of CCS networks that multiple industries can use. The government and public can also act as a major buyer and incentivise market uptake by requiring low-emission goods such as cement or steel.

Strong policy must not only be strong, but also consistent. CCS projects often take up to 10 years from concept to operation. The perceived risk of policy changes can act as a barrier to investors.

Brevik CCS. The facility is part of Norway’s Longship project and the world’s first industrial-scale carbon capture plant at a cement facility. The plant recently started operation and production of net-zero cement by capturing up to 400,000 metric tons of CO2 annually. Photo: brevikccs.com Press & media | Brevik CSS

Carbon leakage in a global economy

The alternative cost for an emitter in Norway and EU is carbon taxes. Since only some countries tax carbon, companies might move their operations elsewhere to avoid paying—hurting local jobs and not reducing emissions. EU is introducing a “carbon border tax” (called CBAM) in 2026 to address this challenge. Imported steel, cement, and aluminium will face the same carbon costs as European-made goods. It is made to create a level playing field and encourages global climate action. Experts predict that even countries like China will ramp up CCS in their industries to stay competitive [2].

Smart policy can help ensure everyone shares the cost—and the responsibility—of cutting emissions. Ideally, carbon taxes and emission standards should be global. A breakthrough in this direction was made earlier this year as a major global draft agreement was reached for the shipping industry [4]. Starting in 2028, ships will need to pay a fee for the CO2 they emit. The aim is to encourage ships to use cleaner technologies and reduce their emissions over time. Money collected from these fees will be used to reward low-emission ships.

A logistic puzzle - Building the full CCS Value Chain

Historically, CCS have found a business case and deployment in especially larger gas processing plants where the CO2 concentration is high, and where gas cleaning has been required to meet a product spec. The captured CO₂ has predominantly been delivered to Enhanced Oil Recovery (EOR) via pipelines. EOR is a technique for increased oil production, whereby CO2 is injected into a reservoir to increase pressure which improves oil extraction. However, in the last decades, a CCS industry is developing where different parties take responsibility for different parts of the value chain, from capture, transport and collection at hub, to storage.

The concept of hubs and clusters has established as the dominating model. Multiple emitters can tie into a shared hub and network where CO2 is consolidated for transport and storage. Such a model enables economies of scale and cost reduction per ton, which clearly is key for a marginal and capital-intensive waste management business.

Author Kari Forthun visiting world's first CCS plant where emitters deliver CO2, Northern Lights in Øygarden, Norway. Northern Lights is part of the government funded Longship project.

CCS as a service cost to the industry

With the hub model, CCS becomes a service cost for the industry. Emitters pay a tariff cost per ton of CO2 disposal rather than building and owning the full CCS value chain. The emitters invest upfront in the CO2 capture plant and its integration only.

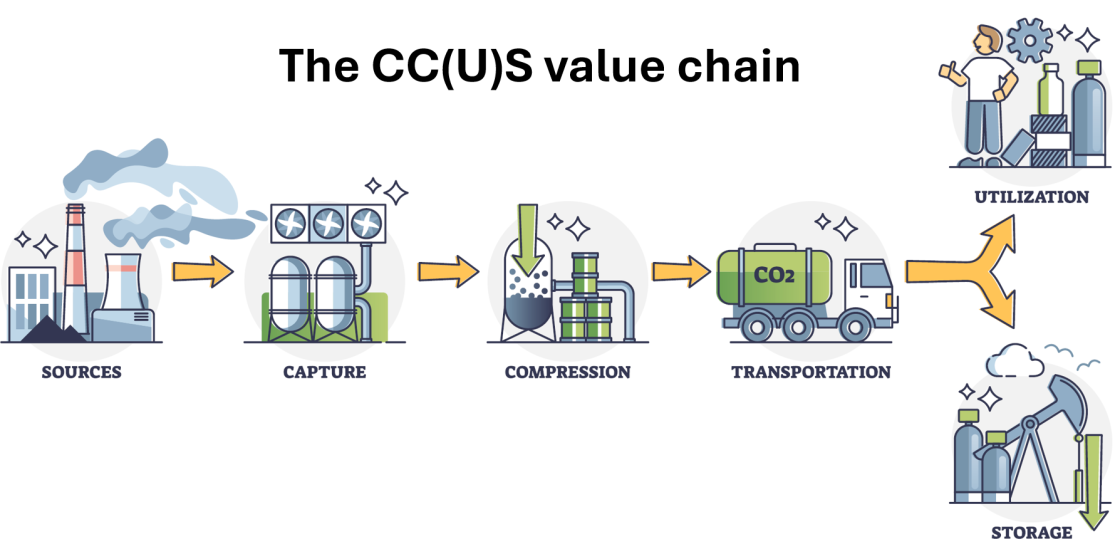

The CC(U)S value chain (Carbon Capture Utilisation and Storage) . Different parties take responsibility for different parts of the value chain, from capture, transport and collection at hub, to storage.

The shared infrastructures should ideally also be designed to accommodate for scaling and larger volumes in the future. The approach enables risk sharing and risk mitigation; however, it also introduces other cross-chain risks related to aligning supply and demand. Contracts and coordination along the value chain are required. An emitter cannot make an investment decision for a capital-intensive CO2 capture plant without confidence that an infrastructure will be ready to bring the CO2 to storage, while an infrastructure and storage provider cannot start to build without commitment from emitters on the delivery of a minimum volume.

Some governments (e.g. UK) have taken an intermediate position and signed contracts that reduce the revenue risk while another approach is a phased build-out. An example of the latter is Northern Lights, that concluded on a phase 2 investment decision and scaling to 5 MTPA in March 2025 [5]).

DRAX power plant in UK, November 2023. The coal fired power plant is transitioning to Bioenergy with CCS enabling negative emissions. UK government is actively derisking the alignment of supply and demand along the value chain by signing contracts that give an emitter and storage provider revenue at agreed date – if the rest of the value chain face delays.

CCS deployment is picking up, but far too slowly

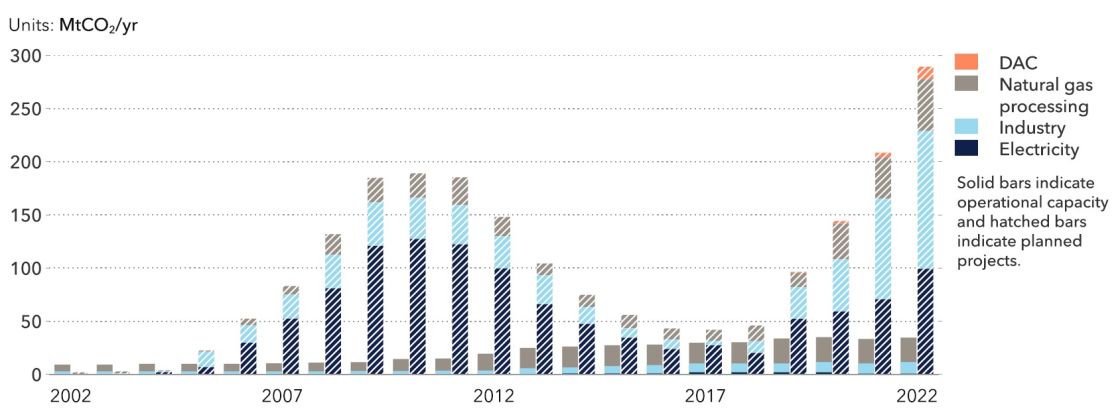

CCS deployment globally is expected to grow ahead. DNV’s recent and ‘most likely’ forecast of our energy system to 2050 predicts growth in stored volumes from today`s 41 Mt/yr to 1.3 Gt of CO2 captured and stored in 2050. This scenario is associated with a 2.2˚C of global warming by 2100 and is far from enough to achieve net zero targets. In net-zero scenarios most models call for 5-6 times more carbon capture by 2050.

Looking back on earlier plans to deploy CCS, most CCS projects in the past has failed, meaning that the planned capture capacity has not been realised. A recent analysis has found that in the first wave of CCS projects in the early 2000s, less than 10 % of the planned capacity was realised [6] . Today, projects are more diversified meaning that CCS is considered for many different applications.

Operational (solid bars) and planned (hatched bars) CO2 capture capacity. Many planned projects in the early 2000s failed to realise, as shown by the first wave in early 2000s. Colours indicate which sector CCS is in use, either capture in Natural gas processing, Industry, Electricity sector or Direct Air Capture (DAC). From DNV CCS outlook to 2050 (figure 3.1) [2].

Policy liftoffs are needed to bridge the gap between actual and required use of CCS to reach net-zero scenarios. This could include

- Higher carbon prices or strict CO₂ limits that make CCS obligatory in key sectors

- Massive investments in CO₂ transport and storage networks

- Innovation funding to reduce capture costs.

Policy should also ensure CCS is used where it makes sense and not to greenwash.

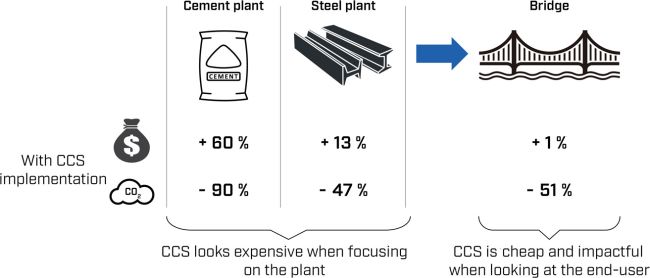

Is CCS expensive?

Dealing with waste always adds cost. The end-user perspective is interesting to consider when evaluating costs and benefits of CCS. Recent studies have investigated the real costs and benefits of CCS from an end-user perspective [7]. Implementing CCS can drastically cut emissions for products like cement and steel by over 50% with only a marginal cost increase for the consumer, often less than 2% for various end-products and services [8]. CCS is cost-intensive at the plant level (larger point sources of emission), but the cost is spread across the supply chain for end-users. As an example, bridge construction costs are found to increase by 1 % only.

Example of end-user perspective on cost of CCS. A study shows that implementation of CCS significantly increases cement and steel costs, but the subsequent increase in the overall bridge construction cost remains marginal at +1 % [7].

In conclusion, CCS doesn’t compete with other climate measures; it complements and completes our aim to cut CO2 emissions. It addresses the “last mile” that renewables and efficiency can’t reach. CO2 utilisation is also a route of interest, however in a climate perspective CO2 must be treated as waste and safely disposed of.

If we treat CO₂ truly like waste, society could decide to scale the waste management accordingly – the same way we invested in sewage systems when cities got serious about public health in the 19th century.

References

[1] «Northern Lights JV has successfully stored first CO2,» Northern Lights JV, 25 August 2025. [Internett]. Available: https://norlights.com/news/northern-lights-jv-has-successfully-stored-first-co%E2%82%82/. [Funnet 29 August 2025].

[2] DNV, «Energy Transition Outlook - CCS to 2050,» DNV, 2025.

[3] DNV, «Energy Transition Outlook 2024, A global and regional forecast to 2050,» DNV, 2024.

[4] I. International Maritime Organisation, «IMO approves net-zero regulations for global shipping,» IMO, 11 April 2025. [Internett]. Available: https://www.imo.org/en/mediacentre/pressbriefings/pages/imo-approves-netzero-regulations.aspx. [Funnet 16 September 2025].

[5] N. L. JV, «Northern lights is expanding capacity through commercial agreement,» Northern Lights JV, 27 March 2025. [Internett]. Available: https://norlights.com/news/northern-lights-is-expanding-capacity-through-commercial-agreement/. [Funnet 10 September 2025].

[6] T. Kazlou, A. Cherp og J. Jewell , «Feasible deployment of carbon capture and storage and the requirements of climate targets,» Nature Climate Change, pp. 1047-1055, 24 September 2024.

[7] S. Roussanaly, S. G. Subraveti, E. R. Angel og A. Ramirez, «Is Carbon Capture and Storage (CCS) Really So Expensive? An Analysis of Cascading Costs and CO2 Emissions Reduction of Industrial CCS Implementation on the Construction of a Bridge,» Environmental Science and Technology, pp. 57,6,2595-2601, 2 February 2023.

[8] S. Roussanaly, T. Gundersen og A. Ramirez, «Putting the costs and benefits of carbon capture and storage into perspective: a multi-sector to multi-product analysis,» Progress in Energy, pp. Vol.7, Number 1, 19 November 2024.

Fjell Tech Agenda is a publication by Fjell Technology Group aimed at sharing knowledge with customers, partners, and stakeholders. Its purpose is to present complex topics in a clear and accessible format for non-experts. The publication is not intended to promote Fjell Technology Group’s products or services. All content reflects the views and insights of the individual author, and Fjell Technology Group does not assume responsibility for the opinions expressed.

Suggestions for future topics are welcome at post@fjelltg.com.

Happy reading!

Kari Forthun, Fjell Technology Group

Kari Forthun is a Chemical engineer driven by a passion for nature and environment. She has more than 12 years of experience, mainly as an assertive and dedicated technology and innovation leader and project management professional.